A Practical Step-by-Step Plan for U.S. and Canadian Investors

If you have $500 and want to start investing in real estate, you’re not alone.

You’ve probably seen:

- Rental income stories

- Passive cash flow examples

- Crowdfunding platforms advertising 8–12% projected returns

But here’s the reality:

$500 won’t buy you property.

It won’t replace your salary.

It won’t generate meaningful monthly income.

What it can do is give you structured exposure to income-producing real estate — without taking on mortgage risk.

Let’s walk through exactly how to do it responsibly.

Step 1: Understand What $500 Is For

With $500, your objective is:

- Learning how real estate investing works

- Gaining diversified exposure

- Avoiding concentrated risk

- Building confidence before scaling

Micro investing is about access — not control.

Step 2: Choose the Right Structure

With $500, beginners in North America typically have three realistic paths.

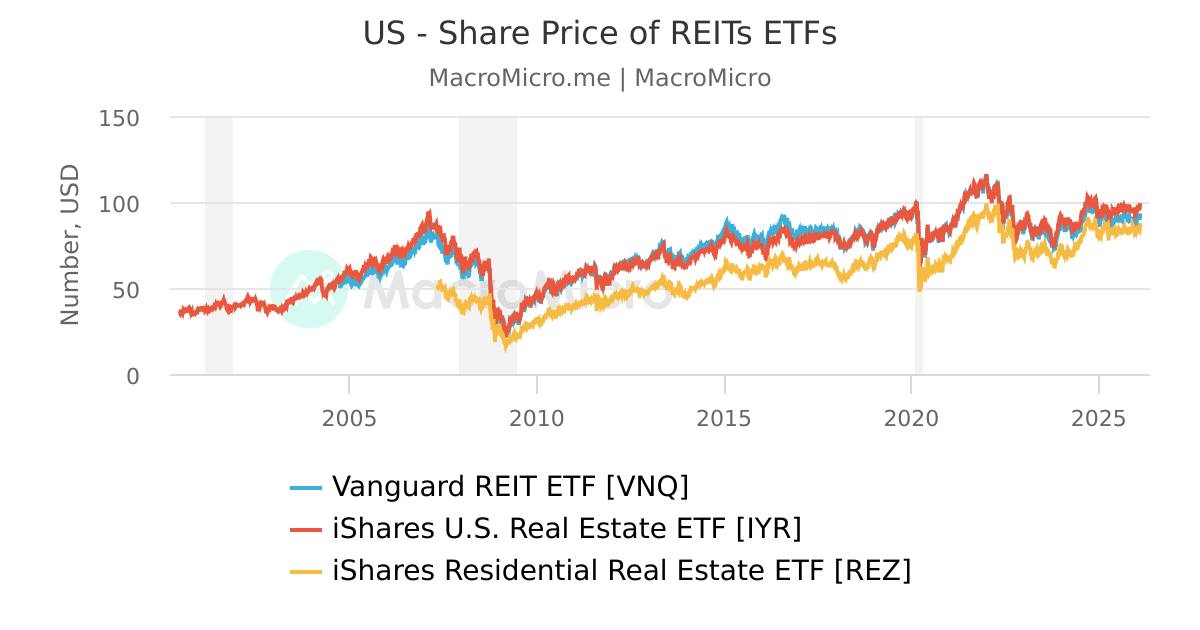

1. Public REIT ETF (High Liquidity Option)

Public REIT ETFs:

- Trade like stocks

- Require very low minimum capital

- Offer sector diversification (residential, industrial, healthcare, etc.)

- Provide dividend income (not guaranteed)

Typical long-term historical return ranges for diversified REIT exposure have generally fallen in the high single digits over long periods, though performance varies by market cycle.

Best for: Beginners who want simplicity and liquidity.

2. Real Estate Crowdfunding (Debt-Focused Deals)

Debt-focused crowdfunding deals:

- Fund short-term real estate loans

- Target yields often range ~7–12% (not guaranteed)

- Usually shorter duration than equity projects

Because these are loan-based, risk is often tied to borrower performance and property collateral value.

Best for: Investors comfortable with limited liquidity and moderate risk.

3. Fractional Rental Equity

Fractional equity investing allows you to:

- Own shares in rental properties

- Receive proportional rental distributions

- Participate in potential appreciation

Holding periods are often 3–7 years.

Liquidity is limited.

Best for: Investors seeking rental exposure without landlord responsibilities.

Step 3: Smart $500 Allocation Strategy

Putting all $500 into one deal increases outcome risk.

A more balanced beginner structure might look like:

- $250 → Diversified REIT ETF

- $150 → Real estate-backed debt crowdfunding

- $100 → Stabilized rental equity deal

This structure provides:

- Liquidity

- Yield exposure

- Property participation

- Risk spreading

Diversification matters more when capital is small.

Step 4: How to Filter Crowdfunding Platforms Safely

This step is critical.

Before investing even $100, evaluate:

✔ Regulatory Status

- U.S.: Are offerings filed under SEC exemptions?

- Are offering documents accessible?

✔ Transparent Performance Data

- Do they show both successful and underperforming projects?

- Are historical returns clearly disclosed?

✔ Fee Structure

- Management fees

- Acquisition/disposition fees

- Platform servicing fees

Small capital can be heavily affected by layered fees.

✔ Risk Disclosure

Reputable platforms clearly explain:

- Market risk

- Construction risk

- Leverage exposure

- Exit timing risk

🚩 Red Flags

Avoid platforms that:

- Promise guaranteed returns

- Emphasize marketing over documentation

- Lack audited reporting

- Provide vague project summaries

In micro investing, capital preservation is more important than chasing the highest advertised IRR.

Step 5: Realistic Growth Expectation

If your $500 averages 7–9% annually:

After 5 years, that becomes roughly $700–$770 before taxes.

Not dramatic.

But it accomplishes:

- Exposure to real estate income

- Portfolio diversification

- Education through real capital participation

Micro investing builds habit and structure.

Step 6: Scaling Plan

Once comfortable:

- Add $100–$200 quarterly

- Increase diversification gradually

- Avoid overexposure to illiquid deals

Consistency matters more than initial capital size.

U.S. vs Canada Considerations

U.S. Investors:

- Some platforms require accredited status

- Tax reporting may involve 1099 or K-1 forms

Canadian Investors:

- Some U.S. platforms may restrict participation

- Currency risk applies

- TSX-listed REIT ETFs may offer simpler domestic access

Always confirm eligibility before funding.

Final Answer: Is $500 Enough?

Yes — if your goal is structured exposure and disciplined growth.

No — if you expect immediate passive income.

Micro real estate investing works best when:

- You diversify

- You understand liquidity limits

- You scale gradually

- You filter platforms carefully

$500 won’t change your life overnight.

But it can change how you build wealth long term.

Start structured.

Stay patient.

Scale intelligently.

If you’d like next:

- Best small-cap crowdfunding platforms (2026 breakdown)

- $500 vs $5,000 long-term modeling

- Risk-adjusted comparison across micro strategies

- Step-by-step account setup walkthrough

Leave a comment